Optimize queries to track trading algorithm performance

0

votes

0

answers

66

views

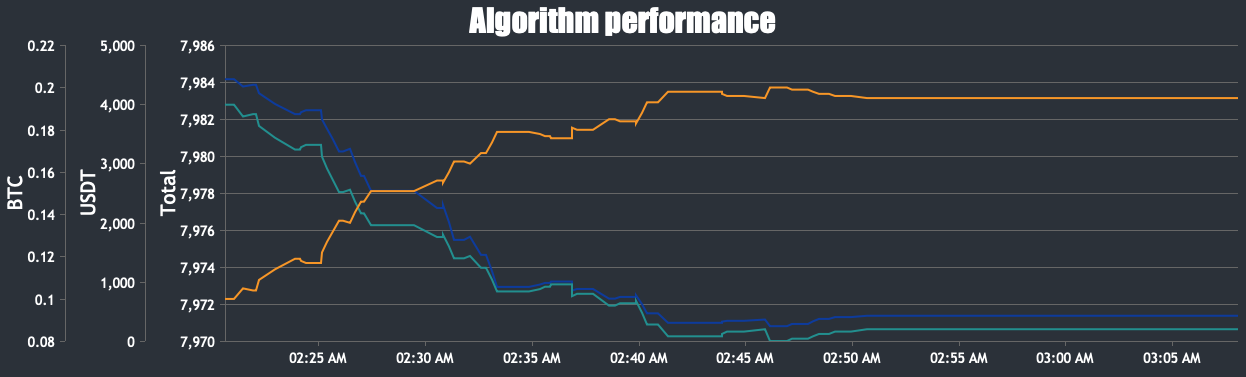

I have a panel where a user can upload Python trading algorithms acting on the Binance API and track the performance of each algorithm in e.g a chart like this:

For each algorithm the amount of BTC, USDT and the total funds (USDT + BTC * actual_btc_price) are displayed.

To achieve this I have the following tables.

**algorithms** - Holding all the algorithms and their configuration.

For each algorithm the amount of BTC, USDT and the total funds (USDT + BTC * actual_btc_price) are displayed.

To achieve this I have the following tables.

**algorithms** - Holding all the algorithms and their configuration.

For each algorithm the amount of BTC, USDT and the total funds (USDT + BTC * actual_btc_price) are displayed.

To achieve this I have the following tables.

**algorithms** - Holding all the algorithms and their configuration.

Table "public.algorithms"

Column | Type | Collation | Nullable | Default

------------------+------------------------+-----------+----------+-------------------------

id | character varying(255) | | not null |

description | character varying(512) | | not null |

start_funds_usdt | numeric | | not null | 0.00

interval | character varying(3) | | not null | '1s'::character varying

run_every_sec | integer | | not null | 0

user_id | integer | | not null |

Indexes:

"algorithms_pkey" PRIMARY KEY, btree (id)

Referenced by:

TABLE "_timescaledb_internal._hyper_4_1_chunk" CONSTRAINT "1_1_history_algorithm_id_fkey" FOREIGN KEY (algorithm_id) REFERENCES algorithms(id) ON DELETE CASCADE

TABLE "history" CONSTRAINT "history_algorithm_id_fkey" FOREIGN KEY (algorithm_id) REFERENCES algorithms(id) ON DELETE CASCADETable "public.history"

Column | Type | Collation | Nullable | Default

--------------+-----------------------------+-----------+----------+-------------------------

algorithm_id | character varying(255) | | not null |

order_id | character varying(12) | | | NULL::character varying

action | character varying(5) | | | NULL::character varying

btc | numeric | | not null |

usdt | numeric | | not null |

btc_price | numeric | | not null |

created_at | timestamp without time zone | | not null | CURRENT_TIMESTAMP

Indexes:

"history_created_at_idx" btree (created_at DESC)

Foreign-key constraints:

"history_algorithm_id_fkey" FOREIGN KEY (algorithm_id) REFERENCES algorithms(id) ON DELETE CASCADE

Triggers:

ts_insert_blocker BEFORE INSERT ON history FOR EACH ROW EXECUTE FUNCTION _timescaledb_functions.insert_blocker()

Number of child tables: 1 (Use \d+ to list them.)# {} is the current btc_price retrieved by the Binance API.

DO

$$

declare f record;

begin

for f in SELECT DISTINCT id from algorithms

loop

insert into history(algorithm_id, btc, usdt, btc_price) values (f.id, 0.0, 0.00, {});

end loop;

end

$$;history even if a order was not made on that minute.

The following issue was that my initial approach was slow: I took the first timestamp available in history for a given algorithm, add a minute to that one until the current time is reached, and in that loop summed all the values of the columns USDT and BTC where the created_at value was lower then the timestamp in the loop.

This was incredibly slow. I solved it by making a view called **history_aggregate**.

CREATE MATERIALIZED VIEW history_aggregate AS

SELECT

created_at,

algorithm_id,

SUM(usdt) OVER (PARTITION BY algorithm_id ORDER BY created_at) AS total_usdt,

SUM(btc) OVER (PARTITION BY algorithm_id ORDER BY created_at) as total_btc

FROM

history

GROUP BY

algorithm_id, history.btc, history.btc_price, history.usdt, history.created_at;WITH btc_price_cte AS (

SELECT btc_price FROM history where algorithm_id = $1 ORDER BY created_at DESC LIMIT 1

)

SELECT

start_funds_usdt + COALESCE(h.total_usdt, 0) + COALESCE(h.total_btc * btc_price_cte.btc_price, 0) AS current_funds_total,

start_funds_usdt + COALESCE(h.total_usdt, 0) AS current_funds_usdt,

COALESCE(h.total_btc, 0) AS current_funds_btc,

h.created_at::TEXT AS ts

FROM

algorithms

LEFT JOIN

history_aggregate h ON h.algorithm_id = algorithms.id

CROSS JOIN

btc_price_cte

WHERE

algorithms.id = $1

GROUP BY

algorithm_id, start_funds_usdt, h.total_usdt, h.total_btc, btc_price_cte.btc_price, h.created_at

ORDER BY h.created_at;

Asked by O'Niel

(61 rep)

Jan 24, 2024, 02:23 AM

Last activity: Jan 27, 2024, 01:38 AM

Last activity: Jan 27, 2024, 01:38 AM